The state of Chinese cloud - Part I

Of installation phases, policy guidance and the industrial internet

This is a new multi-part article on the state of the Chinese Cloud (The State of Chinese Cloud - Part II and III).

Twelve years after its inception, Alibaba Cloud announced the division achieved profitability on the 2nd February 2021. It took AWS 9 years to do the same. Has the Chinese cloud market finally arrived? The short answer is no. The longer answer is it will require more time for the sector to really hit its stride.

| Drawing sky, Cloud drawing, Black pen drawing")

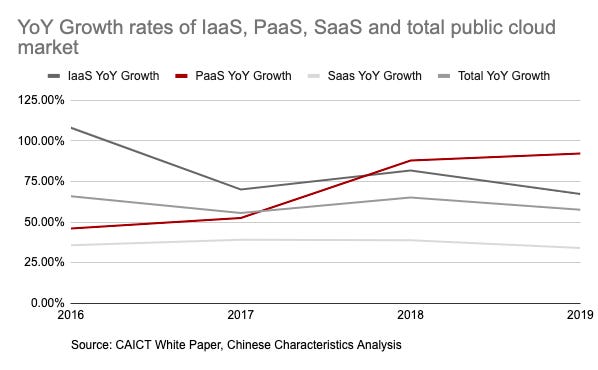

While China's cloud spending is significant in absolute terms, it still lags in relative terms of the US’s total IT spending. Growth has been strong in the last few years but primarily focused on IaaS and private cloud rather than the high business value-added segments such as SaaS or PaaS. Another way to understand this is that the Chinese cloud market is still in its installation phase of cloud and will require additional years to hit its stride in the S-curve adoption.

"Enterprises and especially SMEs, have found implementing infrastructure layer of cloud cannot fully achieve cost reduction and efficiency gains... Due to the lack of talent and technology accumulation, most SMEs have only completed digitalised their infrastructure but have not yet digitised their business processes. This results in limited application usage and affects business use cases not being able to go live in a rapid iteration...The traditional IT departments of SMEs lack experience in the deployment and operation and maintenance of software applications after going to the cloud, resulting in enterprises adopting cloud but not being able to use it well." - Cloud Computing White Paper, CAICT (2020)

Looking forward, Gartner, IDC* and Chinese think tanks such as the China Academy of Information and Communications Technology (CAICT) foresee strong growth in SaaS and PaaS. Cloud market growth ramps up to 28% p.a., reaching a market size of $56.3bn by 2023. As with general cloud market estimations, I'm of the view that this is still an underestimation. Once firms digitise, there is a Cambrian effect of meta-enterprise SaaS tools with no offline equivalent that will expand the market even further.

As I've highlighted previously, the current significant challenges for cloud and SaaS adoption in China are the following:

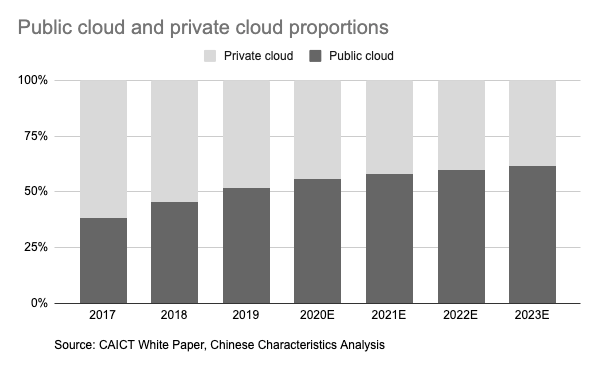

Distrust of public cloud - Cloud is an abstract conception even for the average western firm. On top of the conceptual hurdle of moving one's most precious data to a nebulous ether called cloud, a series of security concern scandals involving leaked data and data loss has made Chinese firms wary about the security of the public cloud. This is why private cloud deployment has been dominant traditionally in China.

Lack of cash and willingness for adoption for SMEs

"Historically, cheap labour in China has meant that manual execution is still very feasible for most tasks, so automating or documenting through software is not a frequent behaviour. Coupled with this, Chinese SMBs generally don't have enough cash reserves to invest in upgrades systematically. When they do have the investment capacity, the prevalence of software piracy in the '00s has led to a general lack of desire to pay for software, and many do not often see value in utilising software" - Why are there no massive Chinese SaaS companies?Enterprises demand high levels of customisation - while large enterprises are willing to pay for digitalisation, they require high levels of hand-holding through the process. They often expect customisation to allow a straight transplant of their existing processes online.

Collectively, these reasons point to a widespread lack of clear ROI for cloud adoption. The traditional cloud migration process assumes an on-premise process foundation in either digital or paper form. This is not the case for the majority of Chinese firms. A McKinsey report on cloud adoption in China noted the need for firms to acquire both software and hardware necessary for the shift. This means a far higher outlay in IT services over the first few years of cloud migration relative to other countries. From a firm's perspective, cloud migration represents an obvious outlay with additional security concerns and unclear up-sides. Even enterprises' insistence on customisation reflects their anxieties against the disruptions the shift may bring.

Besides, the journey of digitalisation but is also the struggle of introducing legibility into the enterprise. Traditional power structures within the firm that derives power from non-legibility (think sales departments that get under the table kickbacks from vendors) will have strong incentives to oppose this paradigm shift.

Tencent echoes these factors in their recent Q4 2020 management call. When asked about the challenges Tencent cloud face while trying to penetrate the enterprise, Martin Lau (President of Tencent) said:

"I would say the No. 1 challenge is really the business reason for them to adopt cloud solutions, right? And that is actually sort of a lot of times the most important question. They may give you the fact that, oh, you may be expensive; they may give you, oh, there's no time and all these other reasons. But the fundamental reason is, OK, what is the key business proposition for converting themselves into a cloud service?

So by having the key business proposition for them to move online and to adopt cloud solutions, I think that's number one. Number two is really inertia, especially more on the organizational inertia, right? All the businesses have their existing practices and suddenly, you say, oh, do you have them all online. Yes, it's more efficient. Yes, it's more cost-effective over time, but it involves the change of behavior of a lot of internal procedures and people's behavior."

But nothing is immutable, least of all in China.

The push and pull factors are already in place; the end of the demographic dividend for the Chinese workforce, the Great Acceleration of COVID-19 towards digitisation, the tech giant's search for new pastures of growth, the desire for technology self-sufficiency in the era of geopolitical tension, the maturation of the enabling factors (or deployment phase if you take Perez's terminology) that would help cloud takeoff. Last but not least, there's the government to help adoption along.

One of the Chinese economy's distinctive attributes is the power of the government's top-down directives. In short, when the centre speaks, the local government, State-Owned Enterprises (SOEs) and private firms listen (though they don’t always follow - “above there are policies; below there are counter policies”). Key government ministries such as the Ministry of Industry and Information Technology (MIIT) and the National Development and Reform Commission (NDRC) presented a series of white papers and policy guidance that encourage the 'digital empowerment of SMEs' by integrating cloud computing. Cloud computing has been elevated to the status of 'new technology infrastructure' in the state OKRs or 14th Five-Year Plan alongside artificial intelligence, blockchain, 5G, IoT and industrial internet to upgrade and transform traditional industries.

These policies are easy to dismiss as the buzzwords of an innovation-anxious nation, but I think they reveal how the Chinese government is rethinking how to approach cloud adoption. The bet here is that given China's comparative advantage in manufacturing, cloud adoption's most explosive opportunities would reside within industries rather than the service sector. With an installation layer of 5G coverage and IoT sensors, cloud computing coupled with edge computing’s processing capabilities and artificial intelligence algorithms, a true industrial internet can emerge.

The vision here is an automated production within an automated factory nested within a network of automated manufacturing hubs. In return for high upfront capital expenditure, efficiency and output will permanently increase through an outward shift of the technology frontier. Labour's role is diminished and needed only for monitoring and servicing. After all, China’s pressing task isn't whether it can get rich before it gets old, but whether it can automate before it gets old.

This is a grand vision, and I've seen many EU governments failing while trying to pursue the same path, so the future is by no means assured. However, the one strength that the focused support of local Chinese governments can provide (and by provide I mean through the carrots of tax breaks and subsidies alongside sticks of withdrawal of bureaucratic support) is that it can help IoT networks reach the level of critical mass needed for the systems to take off. There are significant network effects and spillover effects when entire supply chains are digitised. This aligns with the incentives of both private enterprises and local government cadres who want to see their regions take off.

* I use CAICT’s market-sizing here for a variety of reasons, CAICT is a prominent technical organisation that reports directly to MIIT and their figures therefore those used by the Chinese government bodies to set their targets. CAICT also incorporates Gartner and IDC’s calculations in their work, as well as triangulate that with their own findings and surveys.

Next part in the series: The cloud players and enabling factors

Thanks to everyone who submitted questions for Pinduoduo, the answers will be coming your way soon. Reminder that the premium subscriber deep-dive this month will be on Bilibili.

Good stuff! Thank you